Hi everyone,

Time and again, I’m on the phone with a client of mine answering questions like “Am I automatically enrolled in Medicare when I turn 65?” or “Can I get a Medigap plan at anytime?”.

Let’s clear things up. Check out the most wide-spread Medicare Myths below.

Myth: All Medicare Options are Provided by the Government

No. Medicare is a federal health insurance program, and you can get original (aka, Traditional) Medicare, Parts A and B from the government, but that doesn’t cover all of your medical costs. You can also buy your own Medicare plan from a private company to supplement or replace original Medicare. In either case, most people start the enrollment process when Social Security kicks in.

Myth: The Government Pays for Medicare

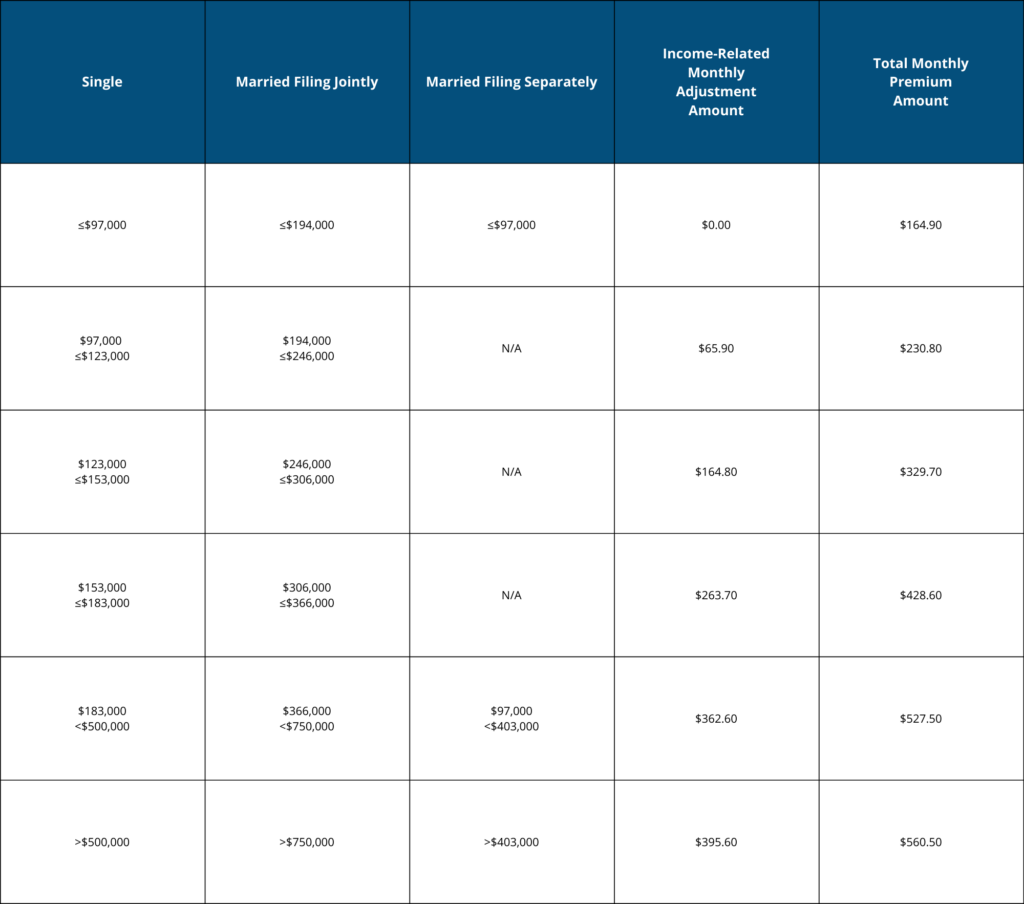

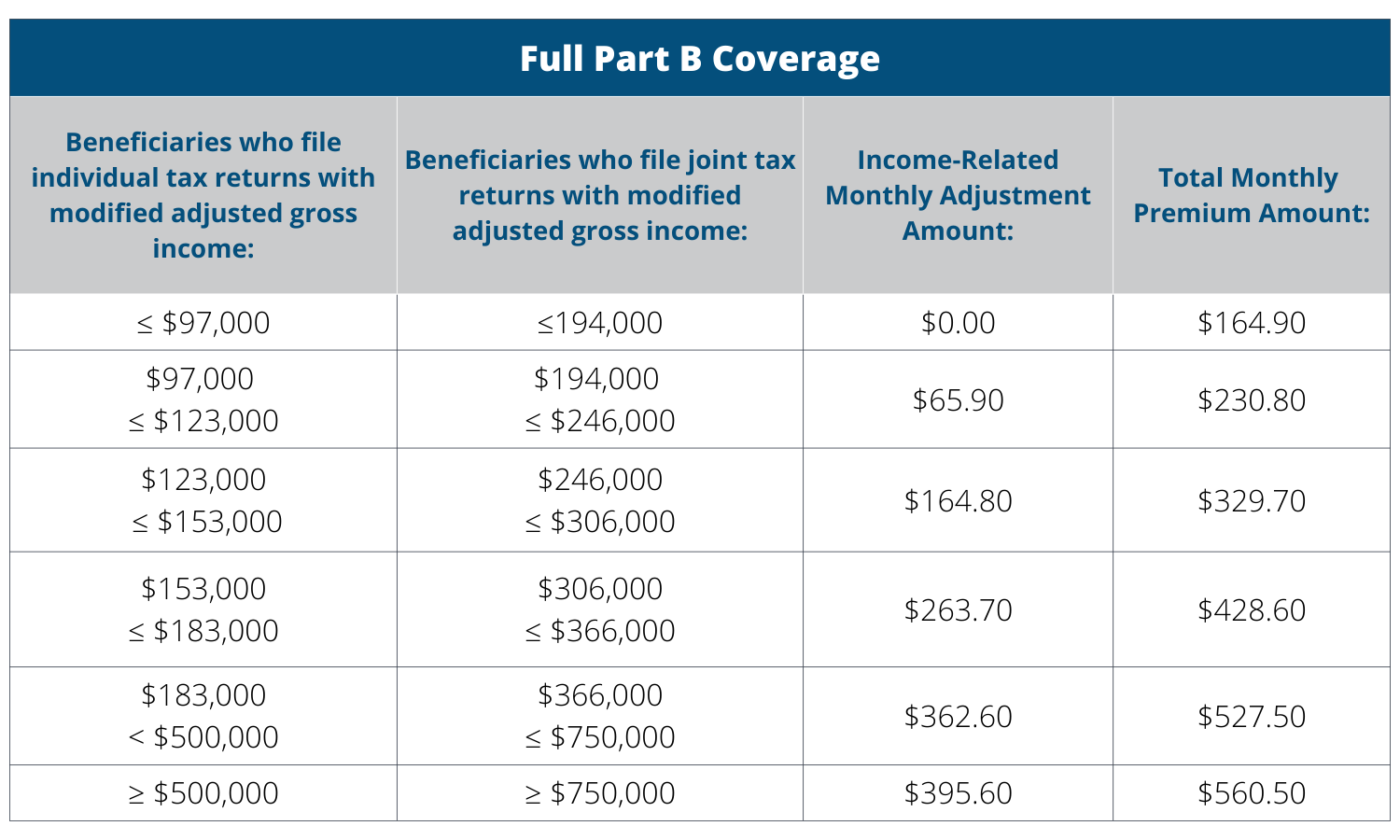

Not really. Most people will be eligible for Part A (hospital coverage) without incurring a monthly premium, but Part B (outpatient coverage), has one. The amount of the Part B premium can vary depending on income level and it will be deducted from your Social Security check if you receive one. If you’re not on Social Security, you will receive a bill.

Myth: You’re Enrolled Automatically at 65

Not always true. Being eligible for Medicare upon turning 65 does not mean you are automatically enrolled. The automatic enrollment into Medicare only happens if you have Social Security when you turn 65. If not, you have to enroll through the Social Security Administration.

Myth: You Can’t Apply Until Your 65th Birthday

Incorrect. When you age into Medicare, your initial enrollment period includes a seven-month period that includes the three months before your 65th birthday, the month of your 65th birthday, and three months after your 65th birthday. If you enroll in the months before you turn 65, your coverage will begin the first day of the month you turn 65.

Myth: You Have to Be 65 Years Old to Receive Medicare

Not completely true. Some people under 65 who have certain disabilities and who have been eligible for Social Security Disability Insurance for at least 24 months as well as with permanent kidney failure, also qualify for Medicare benefits.

Myth: You Have to Wait Until You Retire

False. If you are still working past age 65, it may be beneficial and, in some cases, even required to sign up for Medicare. Even if you will be keeping your employer coverage until you retire, getting Medicare part A makes sense for additional hospital coverage. The decision to enroll in part B as well, depends on the size of your employer and whether you feel that your options in Medicare are better and less costly than your existing employer coverage.

Myth: Medicare Insurance Pays for Every Medical Cost

Not even close. Medical services are subject to copayments, coinsurance and/or deductibles, and original Medicare does not cover vision, dental, or hearing services. Original Medicare also does not have maximum out of pocket limit protection on potential costs, nor does it cover prescription medications. For that reason, it makes sense to consider either a Medigap plan with a stand-alone drug plan or a Medicare Advantage Prescription Drug plan, in order to limit your risk and to maximize your coverage.

Myth: You Don’t Need Drug Coverage

False. Even if you are not taking any prescription medications you should seriously consider enrolling in a Medicare prescription drug plan if you do not have a creditable drug plan already in place. Drug plans are not covered by original Medicare so you can either enroll in a stand-alone, (Part D) drug plan or enroll in a Medicare Advantage plan that includes drug coverage. If you are not enrolled in a Medicare prescription plan of one kind or another, when you are eligible to be on Medicare, without other creditable drug coverage, you will be charged a penalty. That penalty triggers when you do finally enroll in a Medicare drug plan, and it will grow bigger over the period of time you were eligible for it but did not enroll. What’s worse is that it will never go away. This is a permanent penalty that will last as long as you stay on a Medicare Part D prescription plan.

Myth: You Can Get a Medicare Supplement plan (Medigap) Anytime

Sort of true but with a BIG stipulation. Enrollment in Medigap plans is not limited enrollment periods such as the AEP so you can apply at any time throughout the year, but you run the risk of being denied coverage. Medigap carriers can ask medical questions when you are not in your initial enrollment period and they will take into effect any pre-existing medical conditions you have, in deciding whether to approve coverage. For this reason, the best time to enroll in a Medicare supplement plan is during your initial enrollment period (IEP), that runs three months before, the month of, and three months after your eligibility (often your 65th birthday). During that window you will get the best rate possible, and they cannot ask any health questions or take preexisting conditions into consideration. That does not mean you can’t get a Medigap plan outside of your IEP if your health allows for it. Many people regularly shop for a better rate in Medigap plans and they switch when and if they can.

Myth: You Are Allowed to Be Under Your Spouses Medicare Plan, Just Like an Employer Plan

Nope. Medicare is individual and if one partner loses health coverage because a spouse moves to Medicare from an employer plan, then that individual needs to secure their own coverage. Sometimes that may mean enrolling in their Medicare plan depending on age and eligibility and sometimes it requires another option altogether.

Myth: Preexisting Conditions Always Disqualify You From Medicare Plans

Mostly no. Original Medicare and Medicare Advantage plans do not restrict coverage for preexisting conditions and Medigap carriers cannot deny you coverage during your initial enrollment period, (IEP). However, if you want to enroll in a Medigap plan outside of your IEP, you will have to answer medical questions and may be denied coverage. If the Medigap carrier deems that your preexisting conditions will be too costly for them, they can either deny you coverage or charge you much higher rates.

Myth: You Only Get One Chance to Pick a Medicare Plan

Completely false. You can switch amongst or switch to a Medicare Advantage plan every year from Oct. 15 to Dec. 7, which is called the annual enrollment period, AEP. In addition, if you are already in a Medicare Advantage plan and you didn’t switch during the AEP for any reason, you can switch to a different Medicare Advantage or drop your plan and go to original Medicare or a Medigap plan, from Jan. 1 to March 31 every year. Moreover, you can apply for a Medigap plan at any point throughout the year but your acceptance may be dependent on your health.

Myth: You Don’t Qualify for Medicare If You Didn’t Work

That depends. If either you or your spouse paid federal payroll taxes for a minimum of 40 quarters (10 years), you are eligible for Part A with no monthly premium which means you can also enroll in Part B and the other coverage options. If you and/or your spouse paid federal payroll taxes for LESS THAN 40 quarters, are over age 65, and a citizen or permanent resident of the United States, you may be able to enroll in Medicare by paying a premium for part A.

Myth: Dental and/or Vision and/or Hearing (DVH) is Covered by Medicare

It’s all in the wording. Original Medicare (parts A and B) doesn’t cover DVH. That said, many Medicare Advantage plans provide this coverage at no additional cost and if you have original Medicare with a Medigap plan, you can always secure a stand-alone DVH plan with a private carrier to help complete your coverage package.

Myth: I Will Have to Deal with a Provider Network

Not always. Medicare supplement plans are secondary to original Medicare and having original Medicare as your primary insurance means that you can see ANY Medicare provider in the entire country. It’s not going out on a limb to say that most medical providers and facilities in the US take Medicare. Moreover, Medicare providers cannot refuse to accept your Medigap plan as your secondary insurance, no matter who the carrier is, even if they have never heard of the company or don’t take them in a network capacity. On the other hand, most Medicare Advantage plans are HMO’s or PPO’s and/or will otherwise require some adherence to local, regional, or national provider networks.