2023 Medicare Part A and B Deductibles, Premiums, and Medicare Part D Income-Related Monthly Adjustments Amounts

In late 2022, the Centers for Medicare & Medicaid Services (CMS) delivered the dollar amounts for the 2023 Original Medicare Part A & Part B co-insurance, premiums, and deductibles. This article will give you what you need to know about these amounts, how these amounts are calculated, and how these amounts affect Medicare beneficiaries.

Medicare Part B: Premium and Deductible Information and Amounts

Original Medicare Part B is the part of Medicare that covers outpatient hospital services, physician services, some home health services, medical equipment, and other services not covered by Medicare Part A. The prices of the deductibles, coinsurance rates, and premiums for Medicare Part B are settled by the Social Security Act. For 2023, the standard monthly premium for Medicare Part B enrollees is $164.90. All Medicare Part B beneficiaries will also pay $226 for 2023’s annual deductible. These costs are lower than in 2022, primarily because of a larger reserve in the Medicare Part B sliver of the Supplementary Medical Insurance Trust Fund. There is also a small stipulation for Medicare enrollees that are 36 months post kidney transplant, making them no longer eligible for full Medicare coverage. Starting this year, they can pay a premium of $97.10 for coverage of immunosuppressive drugs.

Medicare Part B: Income-Related Monthly Adjustment Amounts

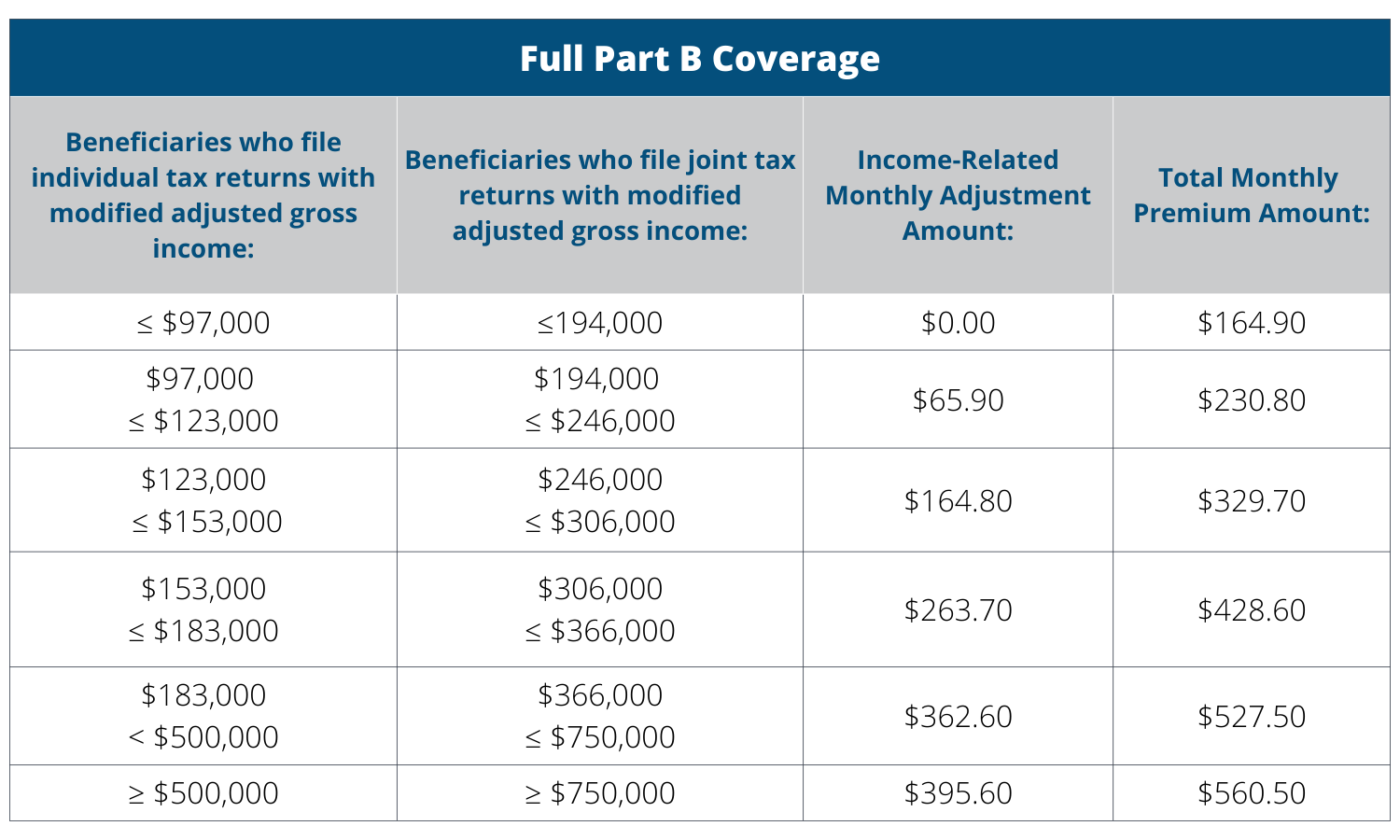

The Medicare Part B monthly premium each beneficiary pays is based on their income. The standard price of $164.90 for 2023 is the price most beneficiaries will pay. Depending on their adjusted gross income, the premium may increase as shown in the chart below.

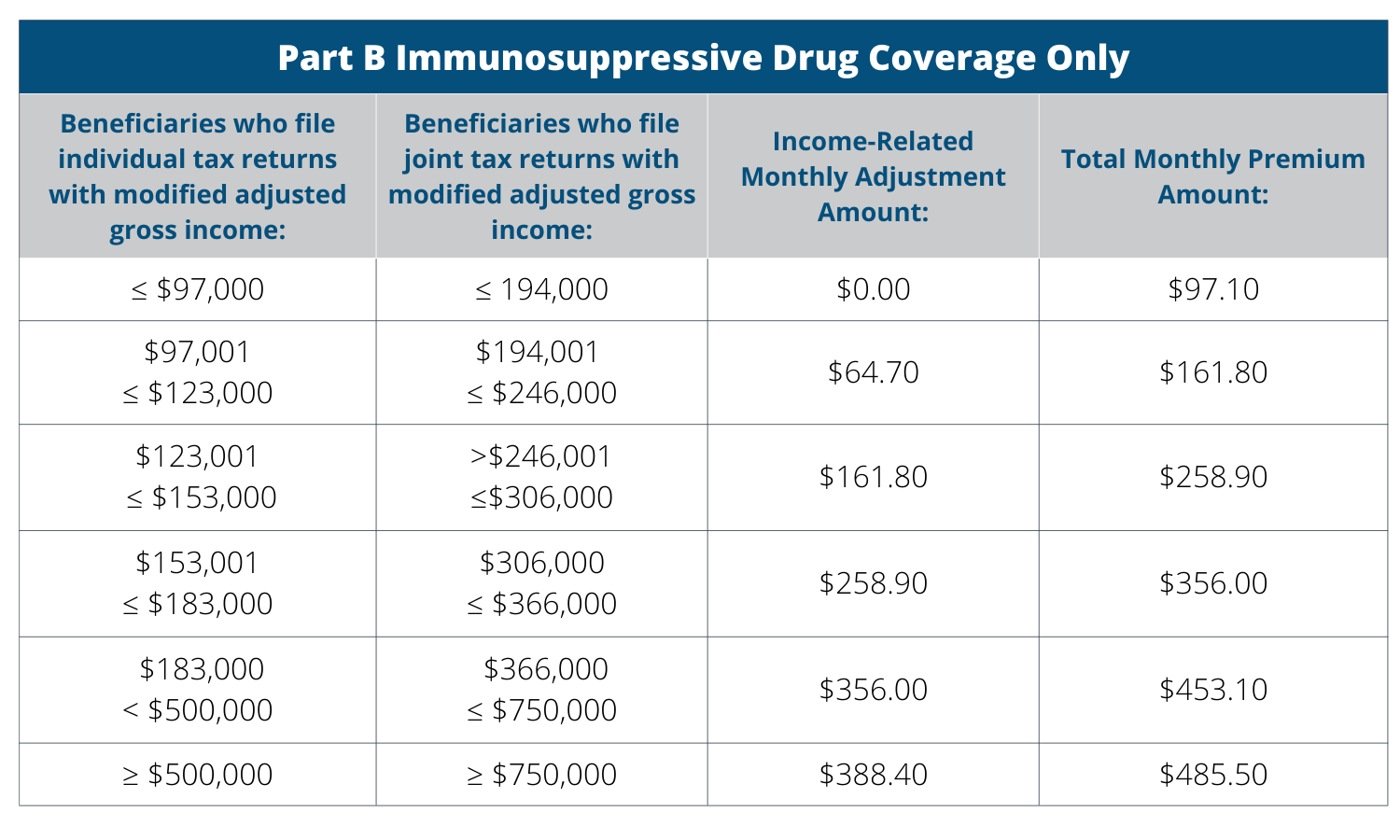

The same levels of adjusted gross income affect the premium the 36-month-out kidney transplant beneficiaries pay for their immunosuppressive drug coverage. The amounts are shown in the chart below.

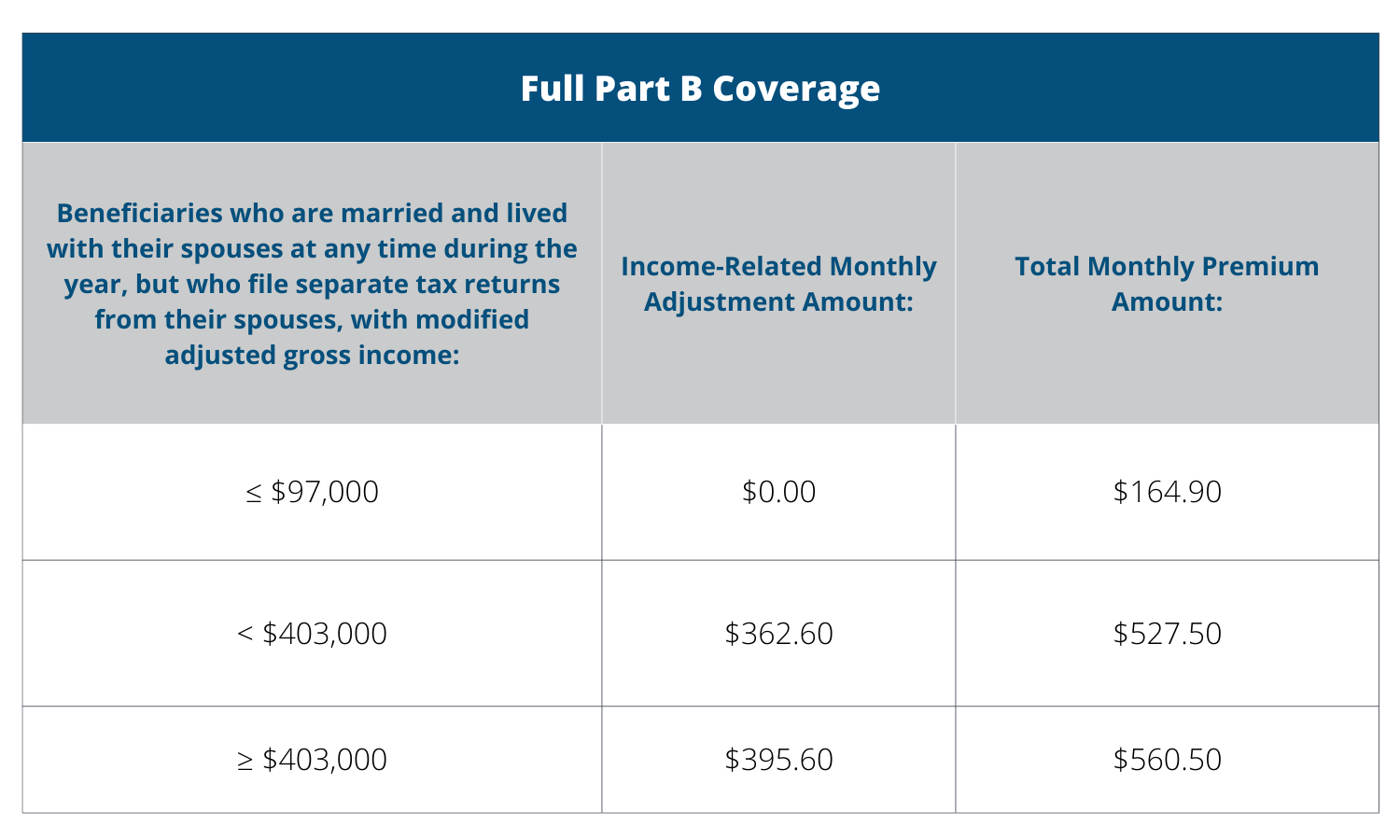

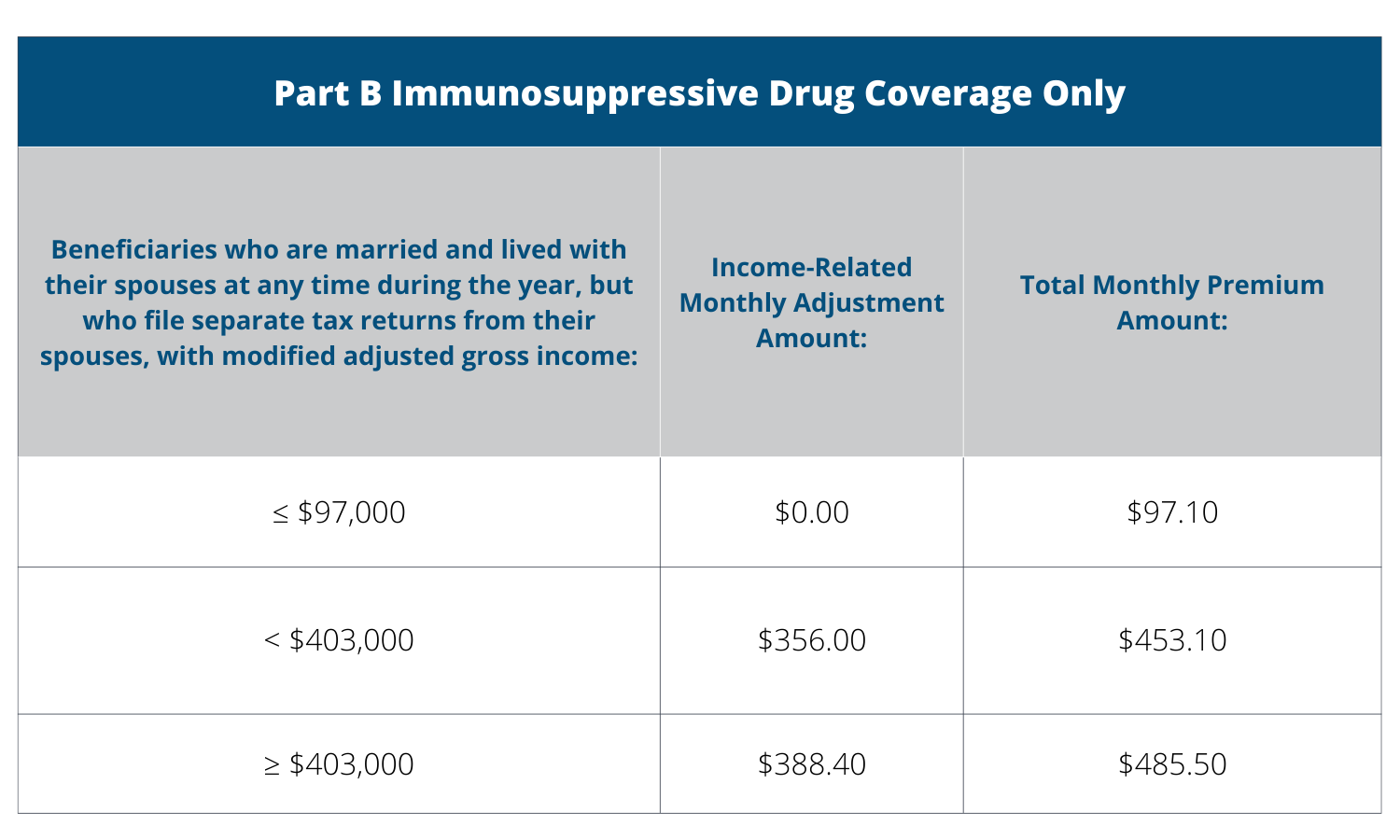

How you file your yearly tax returns can affect these prices as well. Below are two charts respectively showing the two different Medicare Part B premiums discussed above for married beneficiaries who lived with their spouse for any period during the last year but filed a separate tax return.

Medicare Part A Deductibles and Premiums

Original Medicare Part A is the part of Medicare that covers skilled nursing facilities, inpatient hospital stays, hospice, inpatient rehabilitation, and several home healthcare services. Beneficiaries with at least 40 quarters of Medicare-covered employment don’t have to pay an Original Medicare Part A premium which amounts to around 99% of all beneficiaries.

In 2023, the inpatient hospital deductible that Original Medicare Part A beneficiaries will pay if admitted will be $1,600. This deductible covers the beneficiary’s costs for the first 60 days of inpatient hospital care in a benefit period. If any more inpatient hospitalization is necessary in a benefit period, the beneficiary is required to pay a coinsurance amount per day. For days 61-90, the beneficiary will pay a coinsurance amount of $400 per day. If the beneficiary uses any of their lifetime reserve days, they will pay $800 daily. In skilled nursing facilities, days 21-100 of extended care services in a benefit period will require beneficiaries to pay a $200 daily co-insurance.

A monthly premium for Original Medicare Part A is required to enroll in Original Medicare Part A under certain circumstances voluntarily. These circumstances include being age 65 and over and having fewer than 40 quarters of coverage, and certain people with disabilities. If an individual had fewer than 30 quarters of coverage or was married to someone with at least 30 quarters of coverage, they may buy into Medicare Part at a discounted monthly premium rate. This discounted rate in 2023 is $278 per month. Some uninsured aged persons who have less than 30 quarters of coverage will pay the entire premium, which is $506 a month in 2023. If certain individuals with disabilities have drained other entitlement, they will also pay this premium for Medicare Part A.

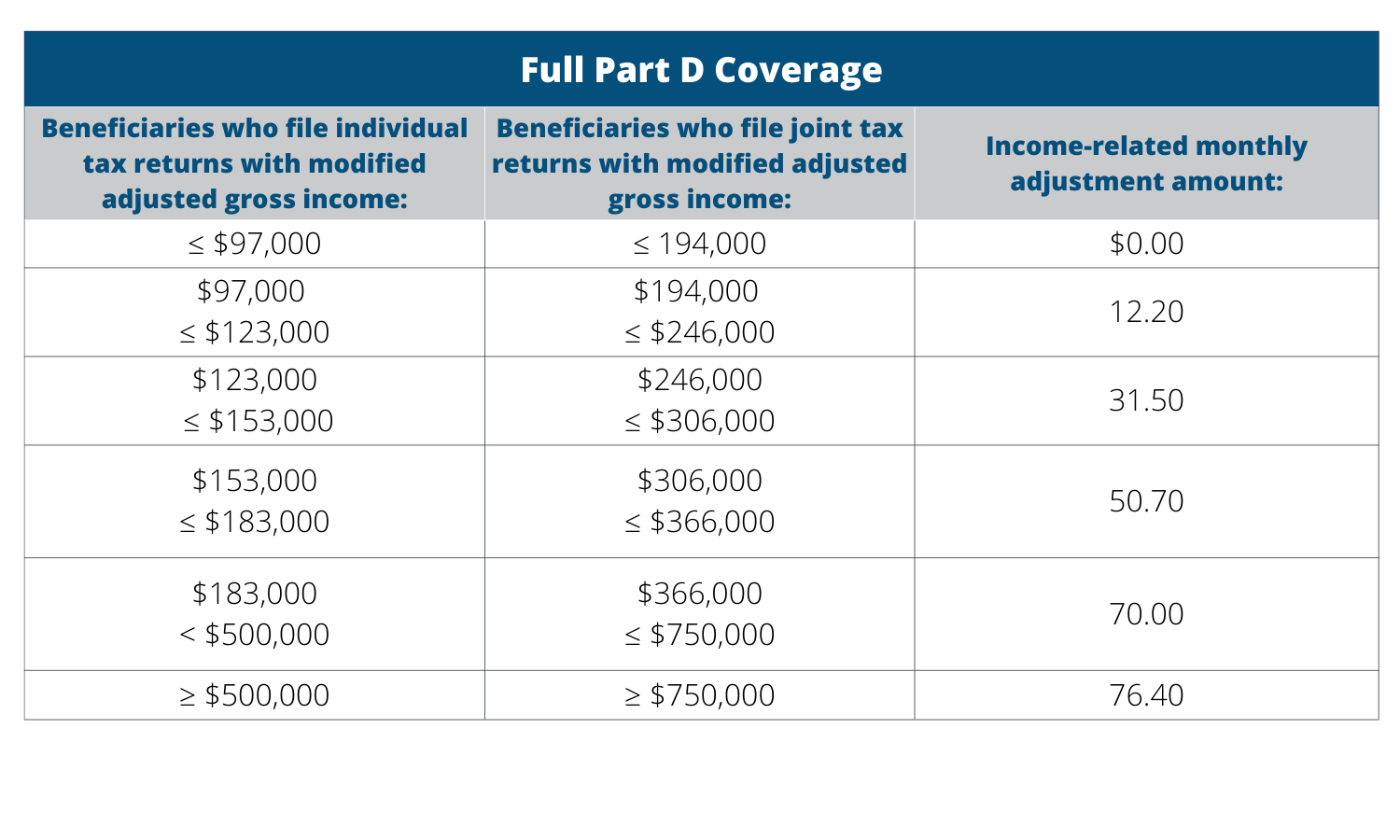

Medicare Part D Prescription Drug Plan Income-Related Monthly Adjustment Amounts

Medicare Part D Prescription Drug Plan premiums depend vary based on the individual plan, but there are income-based adjustments for beneficiaries with a higher income. The income-related monthly adjustment amounts can follow these same payment routes. These amounts are as follows:

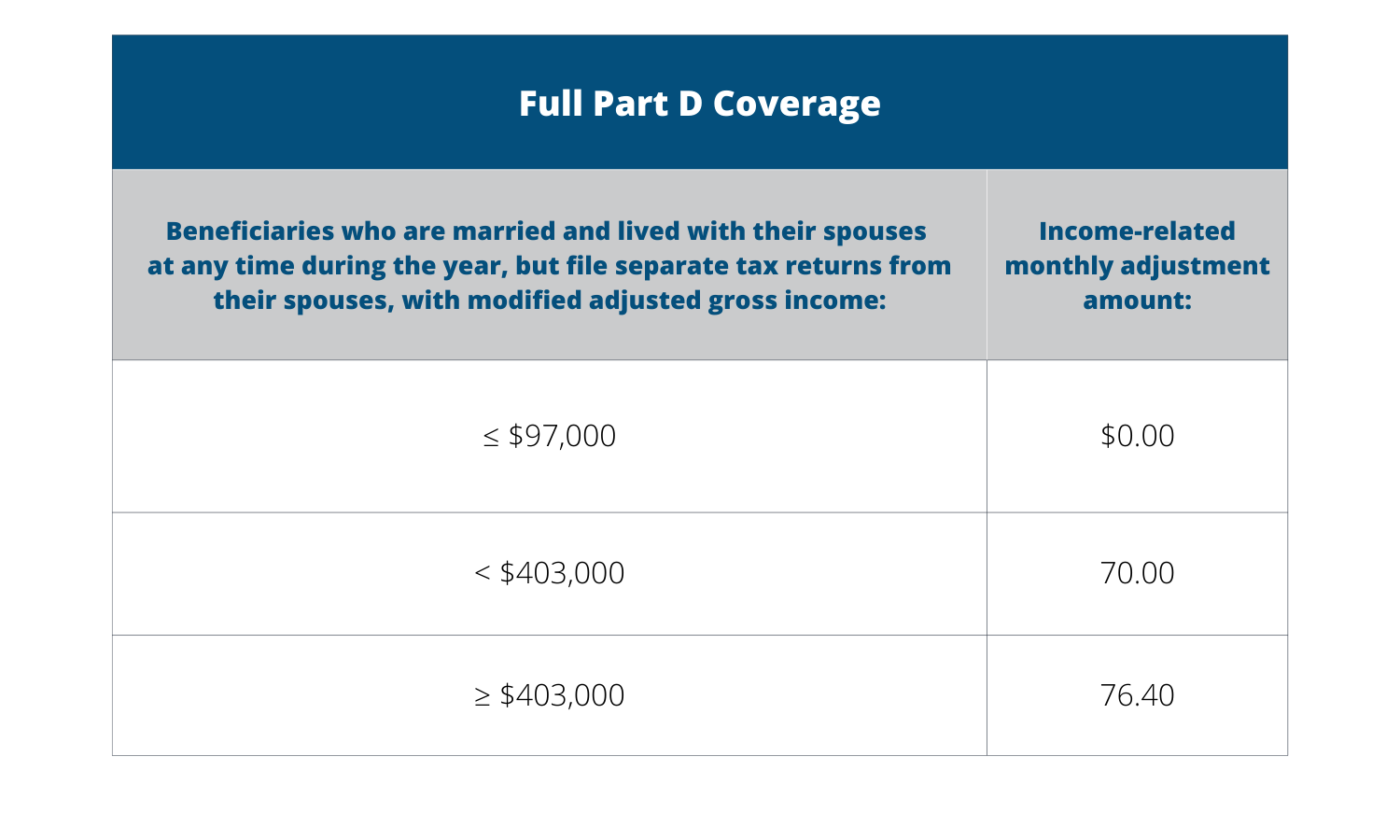

Again, just like Original Medicare Part B, tax returns affect these amounts. Individuals who are married and lived with their spouse for any period of the taxable year but file a separate return will pay different amounts, which are listed below:

Medicare Savings Programs

These deductibles and premiums can add up for extensive hospitalization, specialized care, nursing facilities, etc. For low-income beneficiaries or those on a fixed income, this can be extremely frustrating and difficult to handle financially. However, there is help in the way of the Medicare Savings Programs for some of these individuals. These programs can help reduce the costs of the high-quality care a beneficiary may need. They help pay Medicare premiums and possibly cover co-insurance, deductibles, and co-payments for those who meet eligibility.

For any additional information on Original Medicare Part A & Part B or Medicare Part D Prescription Drug Plan premiums, co-insurance, co-payments, deductibles, or Medicare Savings Programs, contact Seniorstar Insurance Group at 844.779.5010.